The “Eyes” Have It: Turning Robot Vision into Free Shares

It’s March 2026, and the economic headlines are dominated by one word: Reshoring. Under the current administration’s aggressive “Made in America” mandate, factories are sprouting up from Ohio to Arizona. But there’s a catch—Trump’s immigration policies have left these shiny new plants with a massive “Help Wanted” sign and no one to answer it.

If you want to build a car or a chip in America in 2026, you can’t rely on a massive labor pool anymore. You have to rely on a robotic one. And for a robot to do anything useful, it needs to see.

That brings me to my latest move in the Double-Up Free Stock Strategy.

The Trade History: A Slow Cooker Success

I didn’t just jump into Cognex (CGNX) yesterday. This has been a disciplined build since the spring of 2025:

- 04/07/2025: Bought 5 shares @ $24.42 (Total: $122.10). This was the “blood in the streets” entry.

- The Dividend “Peanuts”: Over the last year, I’ve collected three quarterly dividends ($0.40 to $0.43 each). It’s not a yacht, but as the blog says, it’s about the attempt at a free stock while getting paid to wait.

- 03/03/2026 (Today): Sold 2 shares @ $52.3945 (Total: $104.70).

The Math: I’ve almost recovered my entire initial $122 investment by selling just 40% of my position. I still hold 3 shares. If CGNX edges just a little higher, I’ll sell one more, get my initial cash back entirely, and hold 2 shares of a world-leading robotics company for FREE for the rest of my life.

Why CGNX was the “No-Brainer” Buy of 2025

When I placed that buy order in April 2025 at $24.42, the market was terrified. But the fundamentals told a different story.

1. The “Trumpeconomics” Catalyst

In early 2025, the threat of 60% tariffs on Chinese goods and mass deportations was a “risk” to most. To me, it was a “buy” signal for automation.

- Labor Scarcity: U.S. manufacturing wages hit $30/hour in 2025.

- The Math: A Cognex vision system doesn’t ask for a raise, doesn’t need a visa, and works three shifts without a coffee break.

2. AI Hype vs. AI Reality

While the rest of the world was chasing chatbots, Cognex was putting Edge AI into “In-Sight” cameras. In 2025, they launched products that could “learn” what a defect looked like just by being shown 10 good examples. No coding required. This opened up automation to mid-sized factories that couldn’t afford a team of engineers.

3. Valuation & Growth

At my buy-in price, CGNX was trading at a massive discount to its 5-year average. By early 2026, the P/E has stretched to 82x, reflecting the market finally realizing that “Automation is the only way out” of the labor crunch. Revenue is now pushing past the $1 billion milestone, with EBITDA margins expanding toward 25%.

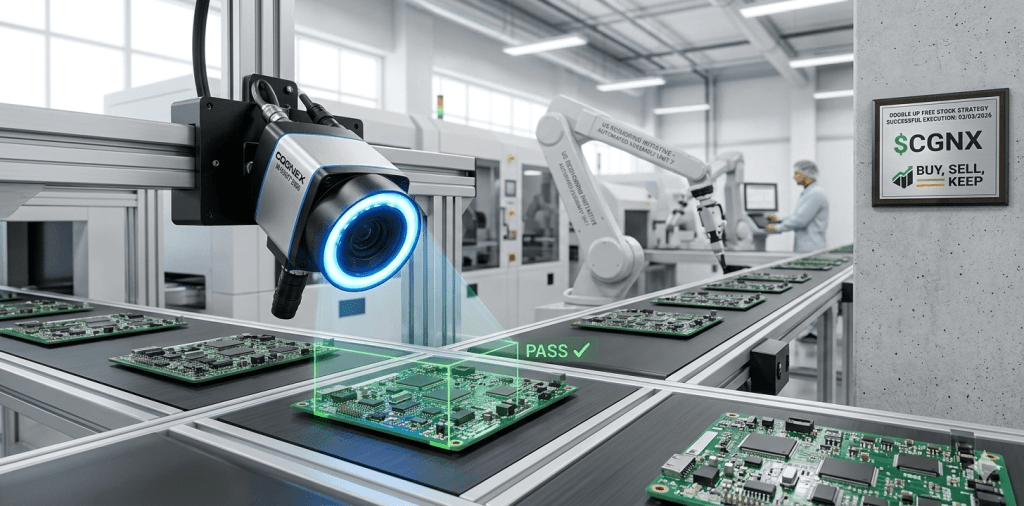

Deep Dive: What Does Cognex Actually Do?

If you aren’t an industrial engineer, you’ve probably never heard of Cognex, but you use their work every day.

The Business Model

Cognex is the global leader in Machine Vision. They don’t make the robot “arms”—they make the “eyes” and the “brains.”

- Identify: Reading barcodes that are torn, skewed, or under plastic wrap (Logistics).

- Inspect: Checking if a smartphone screen has a microscopic scratch (Electronics).

- Guide: Telling a robot arm exactly where a car door is so it can weld it (Automotive).

The Competitive Landscape

Cognex plays in a $7 billion market. Their main rival is the Japanese giant Keyence.

- Keyence is the “sales machine”—they win on sheer volume and speed.

- Cognex is the “tech leader”—they win on the hardest problems. When a task is too “messy” for a standard camera, factories call Cognex.

In 2026, Cognex’s OneVision platform has become the “iOS of the factory floor,” allowing different machines to share visual data. This creates a “moat”—once a factory is running on Cognex vision, switching to a competitor is as painful as switching from iPhone to Android.

Why It Can Still Go Up (Even After Doubling)

You might think I’m crazy for holding my remaining shares after a 100%+ gain. But the “Reshoring” super-cycle is just beginning.

- The “Genesis Mission” Subsidies: The 2026 federal push to bring semiconductor packaging to the U.S. is a direct tailwind for CGNX. These chips are too small for human eyes; vision systems are mandatory.

- Stock Buybacks: The board recently authorized $750 million in buybacks. They are literally using their cash to push my “free shares” higher.

- The “Robot Tax” Hedge: Even if the administration places tariffs on imported robots, Cognex’s high-margin software and AI-licensing model remains protected.

Final Thoughts: It’s Not Just Peanuts

Sure, we’re talking about a few hundred dollars here. But the Double-Up Strategy isn’t about the size of the first bet—it’s about the certainty of the outcome. By extracting my original cash, I am now playing with “house money.”

If Cognex becomes the “Microsoft of Robotics” by 2030, these free shares will be the best “peanuts” I ever ate.

Stay hungry. Stay automated.

Leave a comment