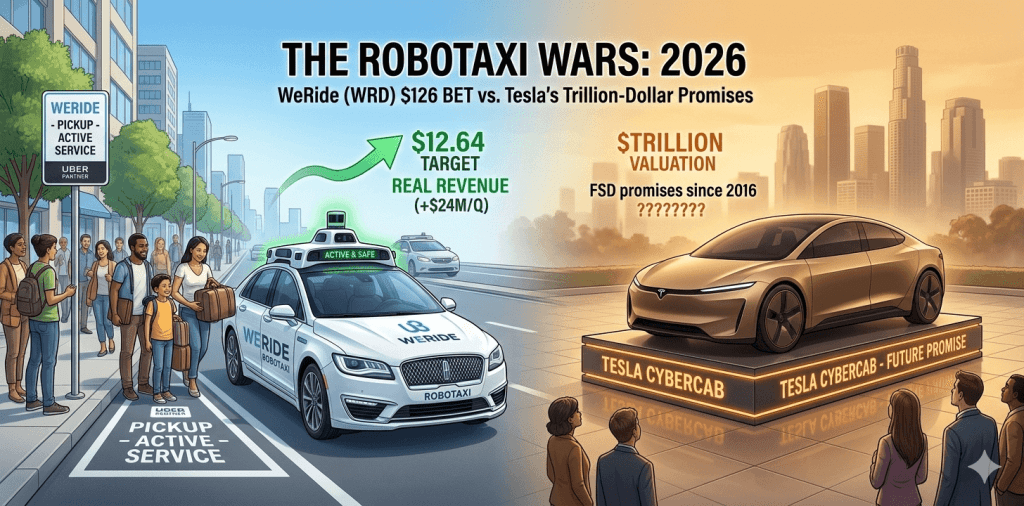

The “Real” Robotaxi Play: $126 to Freedom?

It’s March 4, 2026, and the “Robotaxi Wars” have entered a bizarre phase. On one side, you have Tesla (TSLA), valued at trillions of dollars, still promising that your car will make you money while you sleep “any day now.” On the other side, you have companies you’ve barely heard of that are actually doing the work.

Today, I’m putting a “token” bet on the latter.

Today’s Trade

- Stock: WeRide Inc. (WRD)

- Order: Bought 20 Shares (ADS)

- Price: $6.32

- Total Investment: $126.40

As per the Double-Up Free Stock Strategy, the plan is simple: I wait for WRD to hit $12.64. At that point, I sell 10 shares, take my $126 back, and leave 10 shares in the drawer forever as “Free Stock.”

It’s a tiny amount of money—basically a nice dinner for two—but if this company becomes the “Uber of Autonomy,” those 10 free shares could eventually pay for the whole restaurant.

Why WeRide? (The “Anti-Tesla” Thesis)

I’ll be blunt: betting on Tesla for robotaxis in 2026 feels like betting on a magician who keeps promising to pull a rabbit out of a hat but only produces more hats. WeRide, however, is already showing us the rabbit.

1. It’s “Stupidly” Inexpensive

A few months ago, WRD was trading near $20. Today, I picked it up at $6.32. It’s sitting near its 52-week lows ($6.03), while the broader “Trumpeconomics” rally has pushed other robotics stocks to the moon. This is a classic “Buy the Dip” on a company that the market is temporarily ignoring because it’s not “American Made.”

2. Real Revenue vs. Real Hype

Unlike most autonomous vehicle (AV) startups that are just “pre-revenue” science projects, WeRide is a revenue machine.

- Q3 2025 Revenue: $24 million (up 144% year-over-year).

- Robotaxi Growth: Their specific robotaxi revenue surged 761% last year.

- The Global Footprint: While Tesla struggles with regulatory hurdles in the U.S., WeRide has permits in 8 countries, including Switzerland, the UAE, and Singapore.

3. The Uber Partnership

In February 2026, WeRide and Uber launched a commercial service in downtown Abu Dhabi. This is the “Holy Grail” of the business model: WeRide provides the tech, and Uber provides the millions of riders. They aren’t trying to build a whole new app; they are plugging into the one everyone already uses.

Deep Dive: What is WeRide?

WeRide isn’t just a “taxi” company. They are a full-stack autonomous technology provider. Their business model is a “Dual-Track” strategy:

The Products

- Robotaxi: Level 4 autonomous cars (mostly EVs) running 24/7.

- Robobus: Fully driverless shuttles already operating in places like Singapore and Guangzhou.

- Robosweeper: Autonomous street cleaners. Think about that: a service that cities must pay for, regardless of the economy.

- Advanced Driver Assist (ADAS): They license their “AI Car Brain” to traditional car manufacturers.

The Competitive Edge: The “WeRide One” Platform

The secret sauce is their HPC 3.0 computing platform, powered by dual NVIDIA DRIVE Thor chips. It delivers 2,000 TOPS of AI power. For comparison, that’s enough processing power to “see” and react to a thousand different variables every second.

While Tesla relies solely on cameras (the “Vision Only” approach), WeRide uses a “Sensor Fusion” stack: LiDAR, Radar, and Cameras. In the tech world, this is seen as the “Safer” but “more expensive” route. However, in 2026, China’s supply chain has driven the cost of LiDAR down by 30%, making WeRide’s “safe” tech just as affordable as Tesla’s “cheap” tech.

Why It Can Double ($12.64 is the Goal)

- The “Safety” Premium: As the public gets more nervous about “supervised” FSD crashes in the U.S., the demand for “Level 4” (truly driverless) tech like WeRide’s is going to command a premium.

- Middle East Expansion: The UAE is aiming for 25% of all transportation to be autonomous by 2030. WeRide is the “preferred partner” there.

- The Valuation Gap: WRD has a market cap of around $2.2 billion. Tesla’s market cap has “Robotaxi” expectations worth hundreds of billions baked in. If WeRide captures even 5% of the global market, it’s a $10+ billion company easily.

The Risks (The “Candor” Part)

Let’s be real: this is a $6 stock for a reason.

- Geopolitics: Being a Chinese-linked company in 2026 is like walking through a minefield. Any new “Trump Tariff” or data security law could tank the ADR (American Depositary Receipt).

- Burn Rate: They are still losing money (Net loss of ~$43M last quarter). They have $760M in cash, so they aren’t going broke tomorrow, but they need to reach “escape velocity” soon.

Conclusion: It’s All About the Free Shares

I’m not betting my retirement on WeRide. I’m betting $126. If the “Robotaxi Revolution” is real, WRD is one of the only companies with the permits, the partners (Uber), and the revenue to prove it.

I’ll wait for the double, grab my initial cash, and let the remaining 10 shares sit in the “Free Stock” vault. If they go to zero? I lost a dinner. If they go to $100? They buy me a whole new car (maybe one that drives itself).

What do you think? Is it “stupid” to bet against Tesla, or is it smarter to bet on the tech that’s already picking up passengers?

Leave a comment